![]()

Corporate Transparency Act (CTA): Current Filing Requirements

As of March 26, 2025, the Corporate Transparency Act (CTA) requires only foreign companies registering to do business in the United States to file Beneficial Ownership Information (BOI) Reports with the Financial Crimes Enforcement Network (FinCEN).

Who Must File

-

Foreign companies formed outside the U.S. that register (also called “foreign qualifying”) to operate in a U.S. state or tribal jurisdiction.

-

These entities must report their foreign beneficial owners — individuals who directly or indirectly own or control the company.

Who Does Not Have to File

-

All U.S.-formed companies (LLCs, corporations, partnerships, etc.)

-

All U.S. persons (citizens and residents), even if they own part of a foreign company

-

Foreign entities that fall into an exemption category (e.g., publicly traded companies, banks, insurance firms)

What Information Must Be Reported

Foreign reporting companies must provide to FinCEN:

-

Company details (legal name, jurisdiction, business address, U.S. registration info)

-

Beneficial owner details (full name, date of birth, residential address, and passport or other government ID) — foreign owners only

Deadlines for Filing

-

Newly registered foreign companies: must file within 90 days of registration (reduced to 30 days for companies registering after January 1, 2025).

-

Existing foreign reporting companies: must file by the deadlines set in FinCEN’s compliance schedule.

-

Changes or corrections: must be reported within 30 days.

Penalties for Noncompliance

Failure to file, or filing false information, may result in:

-

Civil fines of up to $500 per day

-

Criminal penalties of up to $10,000 and/or imprisonment

The Evolution of the Corporate Transparency Act (CTA)

-

2021 – Congress enacted the CTA as part of the National Defense Authorization Act to help combat money laundering, terrorist financing, and other illicit financial activity by requiring disclosure of true owners of many companies.

-

January 1, 2024 – The CTA went into effect. FinCEN’s BOI reporting regime launched and both newly formed and existing covered entities began filing Beneficial Ownership Information (BOI) with FinCEN.

-

March 2, 2025 – The U.S. Department of the Treasury announced a reevaluation of reporting obligations following legal and constitutional challenges.

-

March 26, 2025 – FinCEN issued an interim final rule that removed BOI reporting requirements for U.S.-formed companies and U.S. persons. Under that rule, only foreign entities that register to do business in U.S. states or tribal jurisdictions must file BOI, and they must report only their foreign beneficial owners.

If you own a business, or plan on registering one in the future, the Corporate Transparency Act may significantly affect you.

Some significant changes are coming for entities formed or registered to do business in the United States. Congress has passed the Corporate Transparency Act (CTA). The act requires business entities to report their Beneficial Ownership Information (BOI) to the Financial Crimes Enforcement Network (FinCEN). Further, the CTA will affect previously registered/formed companies as it will require them to report their BOI as well.

What is Corporate Transparency Act?

The Corporate Transparency Act (CTA) was passed by congress and left to the Department of Treasury’s Financial Crimes Enforcement Network (FinCEN) to create the rules and guidelines as to how it would be implemented and enforced. The CTA is a part of the Anti-Money Laundering Act contained within the National Defense Authorization Act and its intended creation was “to require certain entities to file reports with FinCEN that identify two categories of individuals: The beneficial owners of the entity; and individuals who have filed an application with specified governmental authorities to form the entity or register it to do business.”

What is the Intended Purpose of the CTA BOI Reporting?

It is believed that this reporting will “significantly enhance the ability to protect the U.S. financial system from illicit use and provide essential information to law enforcement and others help prevent corrupt actors, terrorists, and proliferators from hiding money or other property in the United States.”

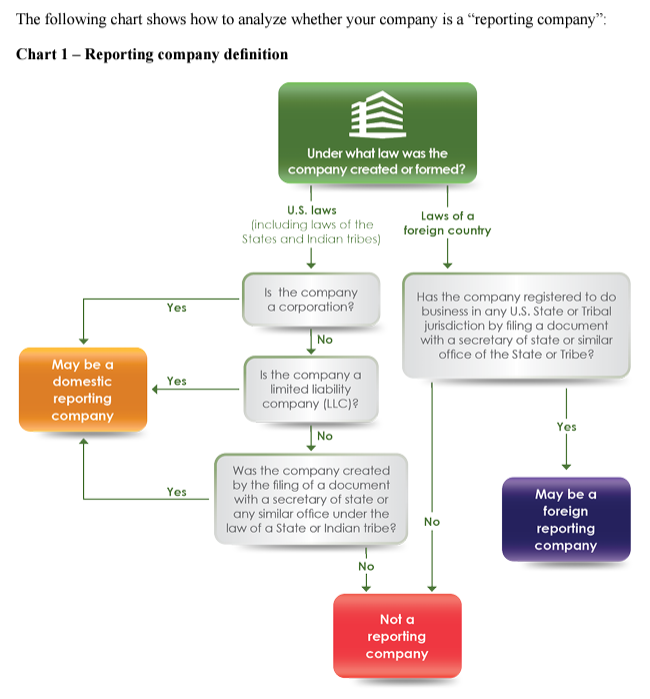

Who Must File?

FinCEN has determined that two types of Reporting Companies must report, Domestic and Foreign.

- A domestic reporting company would include a corporation, limited liability company, or any other entity created by the filing of a document with a secretary of state or similar office under the law of a state or Indian tribe.

- A foreign reporting company would include a corporation, limited liability company, or other entity formed under the law of a foreign country and that is registered to do business in any state or tribal jurisdiction.

What information must be provided?

Information on the Reporting Company, Beneficial Owner and Company Applicant needs to be reported.

Reporting COmpany:

The reporting company, defined above, would need to identify itself by providing their full company name, any trade names or DBA’s, business address, the jurisdiction of formation for a domestic company and the first state of registration for a foreign company and provide the IRS Tax ID number.

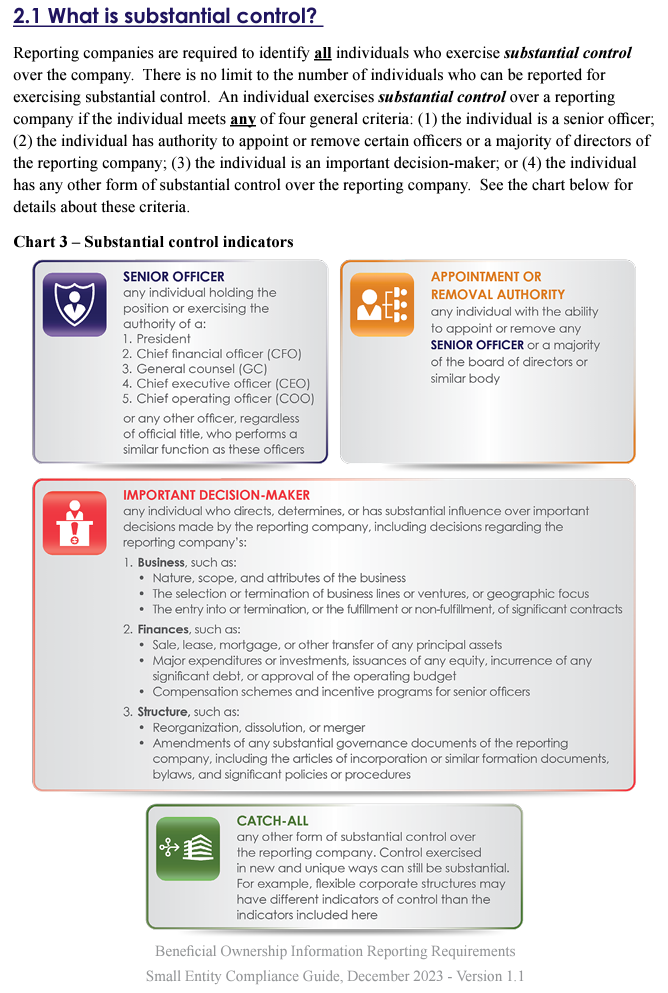

Beneficial Owner:

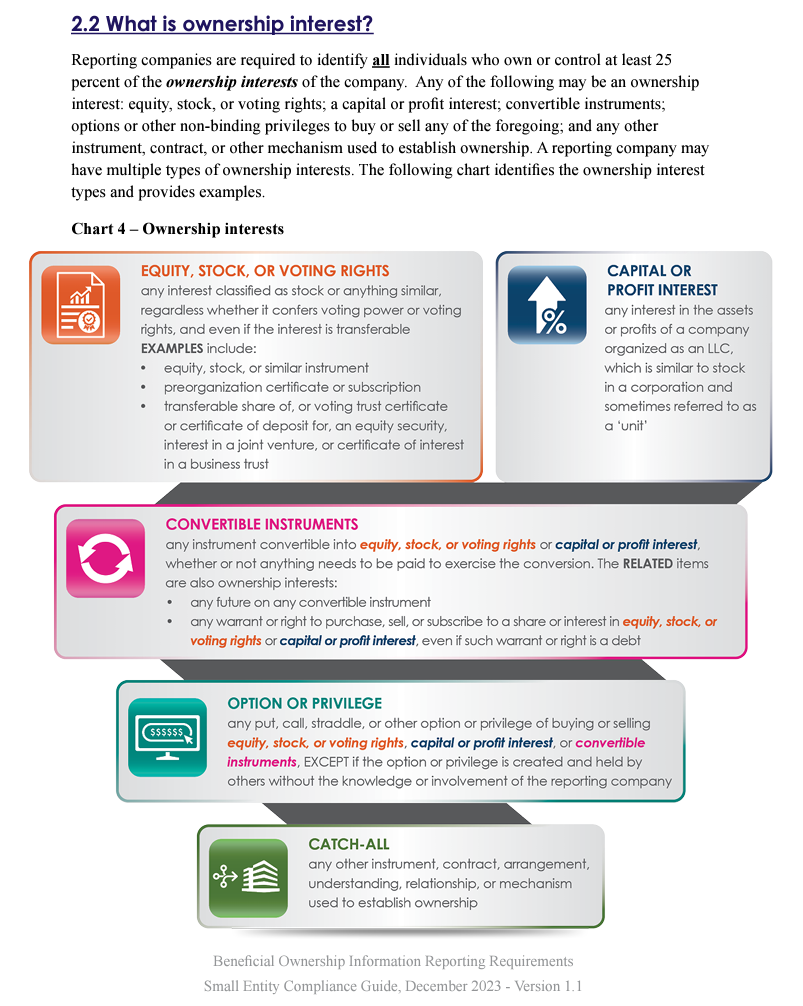

A beneficial owner is any individual who, directly or indirectly:

- Exercises substantial control over a reporting company.

- Owns or controls at least 25 percent of the ownership interests of a reporting company.

- An individual might be a beneficial owner through substantial control, ownership interests, or both.

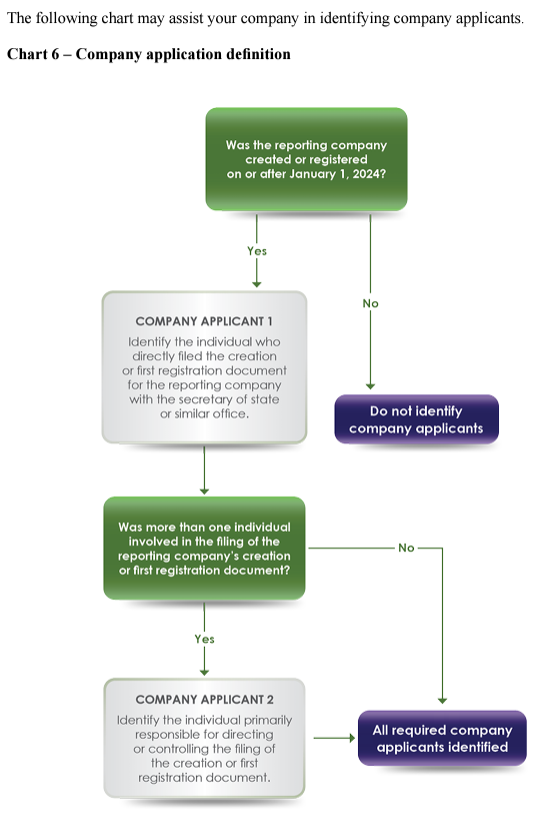

Company Applicant:

- Is any individual who files the document that creates the reporting company, including any individual who directs or controls the filing of such document by another person. (i.e. such as Accumera or an Attorney)

- For a foreign reporting company, a “company applicant” is any individual who files the document that first registers the reporting company, including any individual who directs or controls the filing of such document by another person.

After identifying the Beneficial Owners and Company Applicants the Reporting Company would then report four pieces of information about each:

- Name

- Birthdate

- Address

- A unique identifying number from an acceptable identification document, such as a non-expired passport, government-issued ID document, or driver’s license. (They will also be required to provide an image of the document that contains that unique identifying number and a photo of the individual.)

Note: Company Applicants only need to be reported on Reporitng Companies filed on, or after, January 1, 2024.

When must the BOI be Filed?

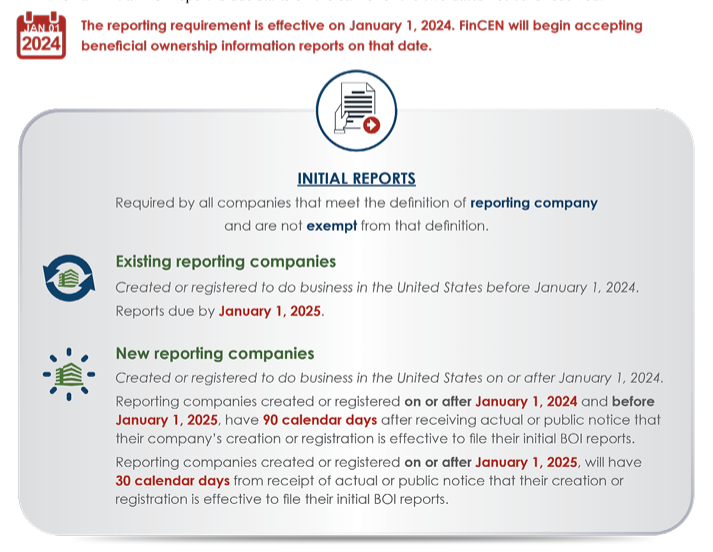

The Reporting Rule is effective on January 1, 2024. FinCEN will begin accepting BOI reports electronically through its secure filing system on this date. BOI reports will not be accepted prior to January 1, 2024. Below explains when your company should file its initial BOI report for Pre-existing companies and new reporting companies.

Preexisting companies will have to file the initial report within one year of the effective date of the new rule.

If your company already exists as of January 1, 2024, it must file its initial BOI report by January 1, 2025. If your company is created or registered to do business in the United States after January 1, 2024, then it must file its initial BOI report within 90 days after receiving actual or public notice that its creation or registration is effective. Please note that this 90 Day extension is only through 12/31/2024, on 1/1/2025 it be 30 days after receiving actual or public notice that its creation or registration is effective.

Previously exempt reporting companies:

Previously exempt reporting companies: If your company previously qualified for an exemption to the reporting company definition but no longer qualifies, you are required to file a BOI report within 30 calendar days of the date on which your company stops qualifying for the exemption.

Exemptions

There are also some companies that are exempt (23 exemptions) from reporting in this manner. Such as companies that already provide information to a relevant government agency heavily regulated companies, and larger companies. The Act explicitly exempts entities such as:

Most financial services institutions, including investment and accounting firms, banks and credit unions, as well as securities trading firms that report to and are regulated by government agencies such as the Securities and Exchange Commission, the Office of the Comptroller of the Currency or the FDIC. Churches, charities, and other non-profit organizations. As well as companies that employ more than 20 people, report revenues of more than US $5 million on tax returns, and have a physical presence in the U.S.

How is the information collected going to be stored or distributed?

FinCEN is required to maintain the information, these reports will collect, in a confidential, secure, and non-public database.

However, FinCEN is authorized to disclose the collected information to [certain government agencies, domestic and foreign, and to financial institutions to assist them in meeting their due diligence requirements. All disclosures of information are subject to protocols to protect the security and confidentiality of the BOI. FinCEN itself is required to establish these protocols].

It is important to know that the CTA does not make beneficial ownership information publicly accessible nor to be queried under the Freedom of Information Act.